Concessional Finance for Addressing Climate Change: A System Ripe for Reform

March 14, 2023

Climate financial intermediary funds (FIFs) represent one of the largest sources of multilateral grant and other concessional finance for climate, including for middle-income countries (MICs). Together, they have received more than $50 billion in cumulative grant funds from donors. They have collectively allocated $48 billion for projects and $2 billion in administrative overhead.

In a new paper, we look at the structure, size, and performance of the three major climate FIFs: the Global Environment Facility Trust Fund (GEF TF), the Climate Investment Funds (CIF), and the Green Climate Fund (GCF). Together, these funds account for more than 80 percent of FIF financing. At a time when grant and concessional climate finance is scarce, the critical question is whether donor resources are going to projects and countries where they are most needed, most impactful, and most catalytic.

Our analysis reveals significant challenges at the systemic level and differing performance across FIFs. Mitigation finance has generally gone to the countries and sectors with the highest emissions, but country mitigation finance volumes are generally not correlated with the size of country emissions. For adaptation finance, the system does not target the world’s most climate-vulnerable countries. None of them is among the top 10 recipients of FIF adaptation finance.

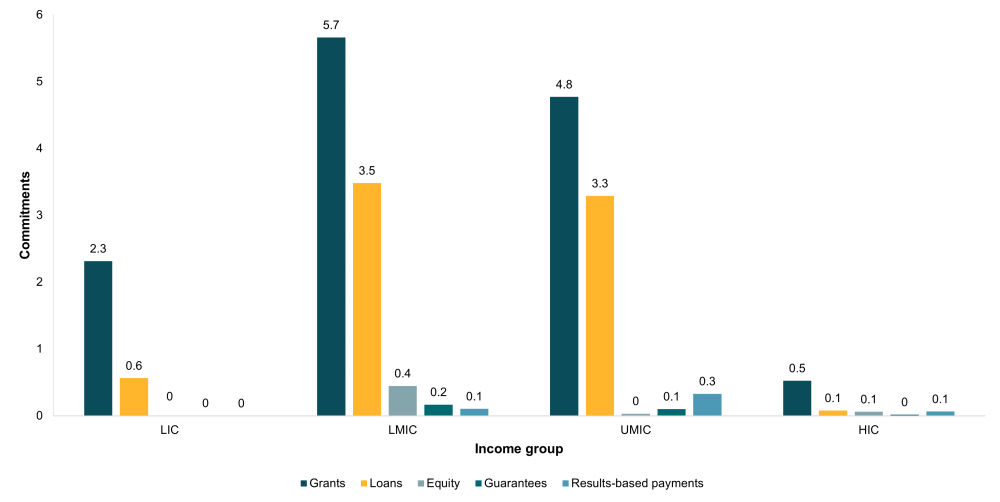

FIFs provide most of their grant and concessional climate finance to MICs, which receive 84 percent of climate FIF commitments. But LICs receive a larger share of their climate commitments in the form of grants (rather than loans, equity, or guarantees). Most FIF financing is in the form of grants (80 percent), and nearly three-quarters go to public sector recipients.

Figure 1. Climate FIF commitment volumes by instrument and country income group (billion USD)

Note: Only includes data from the CIF, GCF, and GEF; estimates are cumulative.

Source: CIF, GCF, and GEF project databases.

Author’s calculations based on project databases.

FIF funding is not allocated according to consistent criteria measuring results and impact, nor are there consistent results and impact reporting standards. Some FIFs report ex ante impact targets; others do not. There is no uniform ex post reporting standard across FIFs based on a common set of core indicators, making it impossible to compare value for money across FIFs. This makes it hard for donors to assess where best to put their scarce grant resources. The evidence, in fact, does not suggest that donors look closely at FIF performance when deciding where to put their funds. For instance, donor contributions to the GCF have grown most rapidly in recent years, though it has been the weakest performer based on the criteria laid out in this analysis.

Unsurprisingly, financing volumes remain very low compared to needs. Overall, FIF commitments of $4 billion per year remain far below levels needed, especially given calls for more concessional lending terms to incentivize more MIC mitigation investment. This volume is clearly also small in relation to overall World Bank Group climate-related finance of $28 billion in 2021 and combined MDB climate-related finance of $50 billion.

The country composition of the FIF donor base is mostly the same as IDA’s and has not changed very much over the past decade. Emerging donors have not stepped up as major contributors. China, for example, could be a significantly larger contributor to climate FIFs, given its importance as an emerging donor and its stake in global GHG emissions reduction.

Finally, climate FIFs vary widely in administrative costs relative to commitments and relative to project numbers. Some ratios of cumulative administrative expenses relative to commitments range up to 20 percent, while others are in the low single digits.

Making the climate FIFs work better

Clearly this is a system ripe for reform, and in our paper, we lay out a series of options. There is opportunity to capitalize on the MDB reform agenda. We propose consolidating the FIF architecture and merging some of the stronger performers into a single independent climate entity. We think that this could better service recipient countries and implementing agencies, strengthen finance allocation, consolidate administrative expenses, rationalize and simplify fundraising, and combine and scale complementary projects.

But key to getting climate finance right is establishing efficient models for allocating concessional resources and grants—especially if middle-income countries are to obtain a larger share for mitigation. We recommend that FIFs adopt common allocation criteria covering:

- projected mitigation and adaptation impact

- the scale of impact relative to country goals and challenges

- the country’s need for concessionality

- for mitigation projects, the project’s contribution to global emissions reduction

- for adaptation projects, the country’s global vulnerability ranking

Allocation methodologies should aim to both maximize ex ante mitigation and adaptation impact and maximize impact per dollar committed. This would require agreement across the FIFs and entire MDB sector on a common methodology for projecting and reporting emissions and adaptation impact and for assessing the need for concessional finance.

And finally, donors and FIFs alike should take issues of financial efficiency seriously. There is a clear tradeoff between terms and volumes which will vary across recipient countries, and getting that equilibrium right will require flexibility and new tools. Except for the CIF’s Capital Market Mechanism, the climate FIFs have not sought to innovate their financial model.

There is strong merit to exploring other ways to deploy FIF financing. For instances, FIFs could consider pooling some of their funds to issue guarantees of some share of climate-related MDB portfolios. That would free up MDB capital and allow use of leverage to generate multiples of that additional capital in more climate lending capacity. Such guarantees at the portfolio level are a more efficient way to expand the impact of donor resources than a cash-in/cash-out approach or a transaction-by-transaction approach. And donor contributions can also be used at the portfolio level to make MDB lending more concessional by blending MDB hard loan resources with grants.

Donors and recipient countries alike need an efficient system that allocates finance faster and evaluates value for money more consistently, so that climate financing is put to optimal use in the countries that need it most. To see our analysis and full set of proposals, please read our paper here.

Learn more