Debt Suspension Clauses to the Rescue?

June 16, 2023

In a recent post, we explored options for scaling Debt Suspension Clauses (DSCs) beyond small island states. (DSCs allow countries to suspend debt repayments for a predefined period following a natural disaster.) In this note we assess the potential short-term fiscal impact of these instruments. We look at three major natural disasters over the past two years and assess how much relief each country would have received if DSCs had been included in the totality of their external debt instruments. The key questions we explore are:

- Would the relief have been commensurate with the financial need associated with the crisis?

- Where would the greatest source of relief have come from?

We find that:

- Payment relief afforded by DSCs can be quite significant relative to the economic impact of the natural disaster if all creditors participate.

- DSCs are less relevant for vulnerable low-income countries with low levels of debt service.

- DSCs are not the right instrument for countries with broader debt solvency issues since they provide short-term liquidity relief but do not reduce the overall size of a country’s external debt.

- Bullet bond repayments structures—which are commonly employed across low- and lower-middle income countries—are not well suited for DSCs.

DSCs 101

DSCs are features in loan contracts that allow a country to temporarily pause external debt servicing if a pre-defined shock hits. By allowing countries to temporarily stop paying creditors in the event of a natural disaster, they free up liquidity that the government can then use to respond to the disaster and its aftermath. While DSCs are having their moment in the global development finance spotlight, from the Bridgetown Agenda to the upcoming Macron Summit, they remain rare in sovereign debt contracts.

To date, only Grenada and Barbados have incorporated DSCs across most of their external debt stocks. In its 2014-2015 restructuring, Grenada succeeded in implementing DSCs in its entire restructured public debt stock, including both private and official bilateral debt. Barbados retrofitted all its bonds with DSCs its 2018-2020 restructuring, and its loans from the Inter-American Development Bank (IADB) also now benefit from DSCs. IADB designed these clauses so that debt service deferral, if triggered, will not be interpreted by credit rating agencies as a credit event, which was a key concern that limited country engagement in the Debt Service Suspension Initiative. However, so far, IADB is the only multilateral development bank (MDB) to the offer them, meaning that both Grenada and Barbados’ World Bank and other multilateral debt does not benefit from DSCs.

Both countries are good candidates for DSCs because they enjoy intermittent capital market access and face a strong likelihood of a predictable natural disaster (think hurricane). Research for a UK-convened working group found that the inclusion of DSCs did not drive up Barbados or Grenada’s market borrowing costs, but given the small sample size it is difficult to extrapolate beyond these cases.

The same working group also found that DSCs are most suitable for low-income countries, small island developing states, and other developing countries particularly vulnerable to the impacts of climate change that do not benefit from sustained market access. They are less relevant for countries with low levels of debt and big issuers with an established market presence that can easily secure extra liquidity through the market.

Box 1. Five Key Facts about DSCs: Designed to provide breathing room to mount crisis response, not a long-term debt workout

- Deferral is net present value (NPV) neutral, meaning creditors are repaid in full without any write-off

- Deferral is time-bound, typically for a maximum of two years per deferral

- Deferral generally cannot be triggered within proximity of maturity (so as not to extend the maturity of the debt)

- Trigger must be predefined

- The clause cannot be implemented on an ex-post basis (i.e., after a disaster strikes)

DSC country case studies: Is relief commensurate with the size of the emergency?

Our case studies look at Pakistan, Mozambique, and Haiti—three countries that do not have DSCs but could have benefited from them after experiencing natural disasters that inflicted severe economic damage.[i] We then estimate how much additional fiscal space would have been freed up over a two-year period under the hypothetical scenario that their entire external debt stock contained DSCs.

For most categories of debt, we included both the principal and interest paid in that year using World Bank IDS data. We excluded bond principal “bullet” payments because deferring these, which occur at the end of the instrument life, would be equivalent to providing a maturity extension (i.e., debt restructuring), which is not a feature of DSCs.[ii]

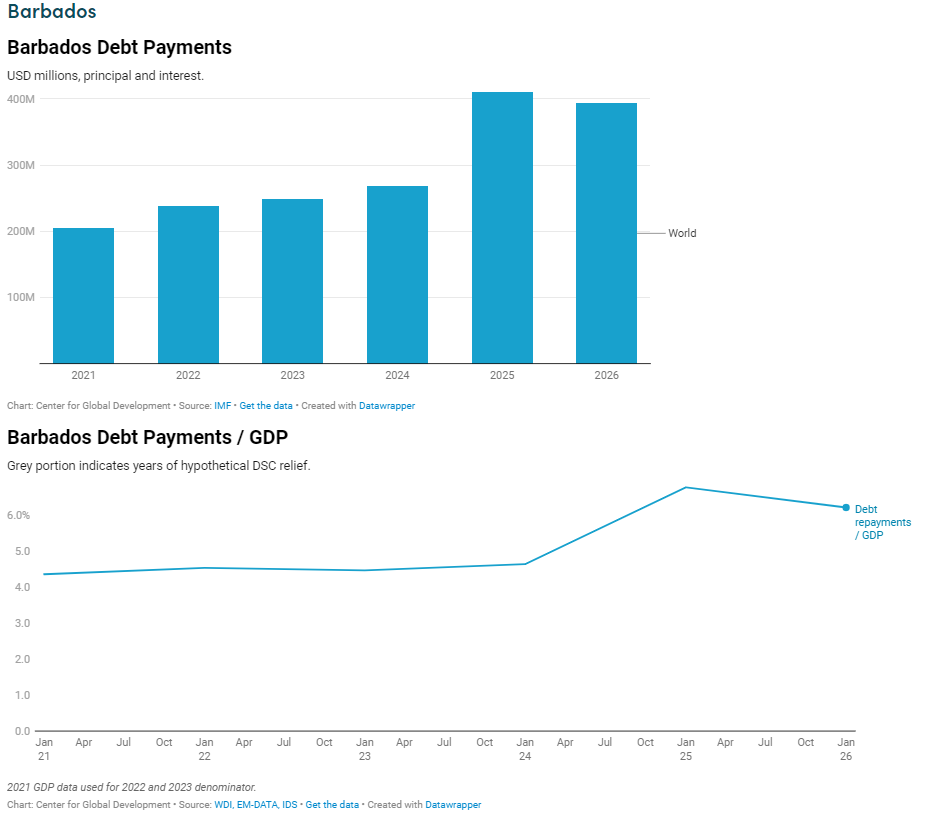

Following its restructuring in 2018-2020, Barbados included DSCs across nearly its entire external debt stock—including commercial as well as some multilateral debt from the IADB. Though its debt is now “stormproof,” these DSCs so far have not been triggered by a hurricane.

Barbados lacks IDS data, so we instead approximated debt service projections using data from its most recent IMF Article IV staff report. These projections suggest that pausing all of Barbados’ debt payments in 2024 and 2025 would result in fiscal space of around 11 percent of GDP.[i] (Given that some of these payments are owed to the World Bank, which does not offer DSCs, the figure is likely slightly lower.)

| Creditor Type | Percentage of relief provided |

| Multilateral | 20% |

| Bondholders (interest only) | 4% |

| Paris Club | 13% |

| China | 51% |

| Other bilateral | 12% |

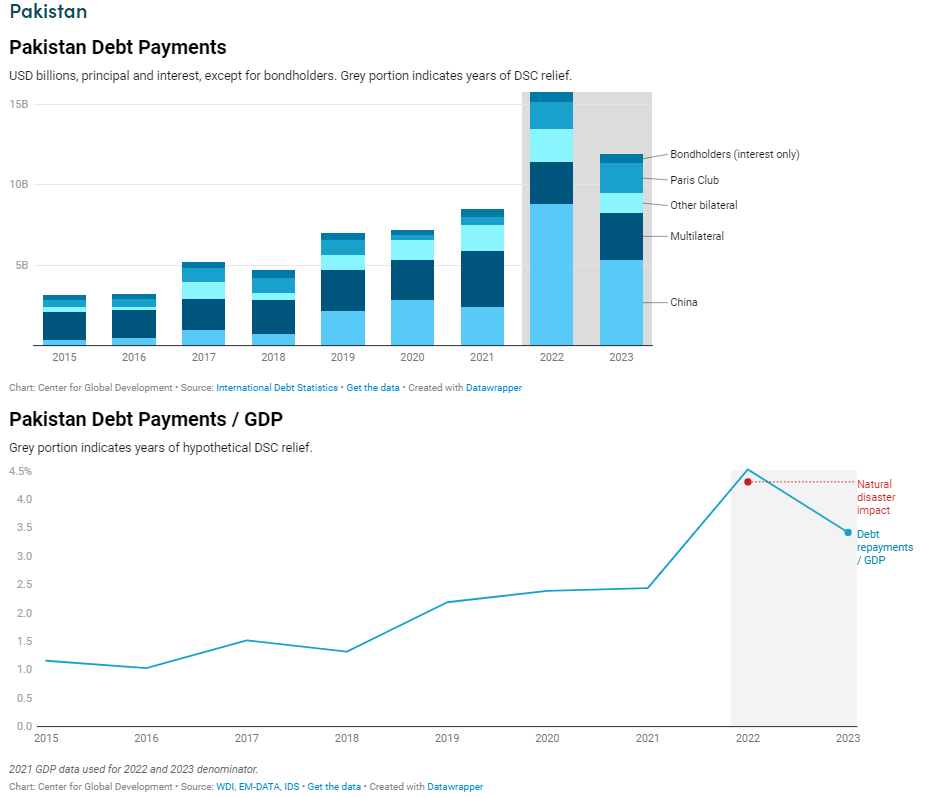

Pakistan’s floods in 2022 inflicted damages estimated at around 4.3 percent of GDP. With a high external debt-to-GPG ratio, Pakistan’s external debt payments accounted for approximately 4.5 percent of GDP annually, meaning that a two-year hiatus could have freed up more than double the estimated amount needed to cover recorded damages. Most of the hypothetical payments pause would have come from China, and only a small fraction would have come from bondholders’ foregone interest payments.

| Creditor Type | Percentage of relief provided |

| Multilateral | 15% |

| Bondholders (interest only) | 6% |

| Paris Club | 49% |

| China | 20% |

| Other bilateral | 10% |

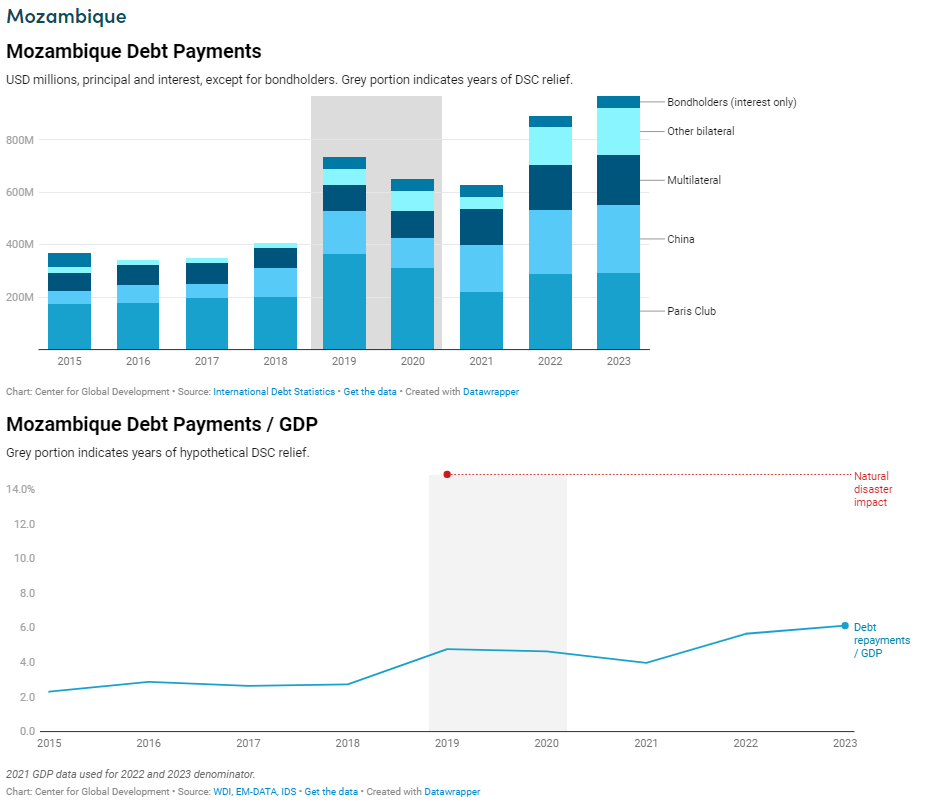

Mozambique’s 2019 tropical cyclone inflicted damages close to 15 percent of GPD. The country’s external debt repayments in 2019 and 2020 accounted for 4.8 and 4.6 percent of GDP respectively. This means DSCs could have freed up as much as 9.4 percent of GDP—not commensurate with the size of the economic losses but still a significant sum. A plurality of the hypothetical payments pause would have come from the Paris Club, and again, only a small share from bondholders in the form of foregone interest.[i]

| Creditor Type | Percentage of relief provided |

| Multilateral | 21% |

| Other bilateral | 79% |

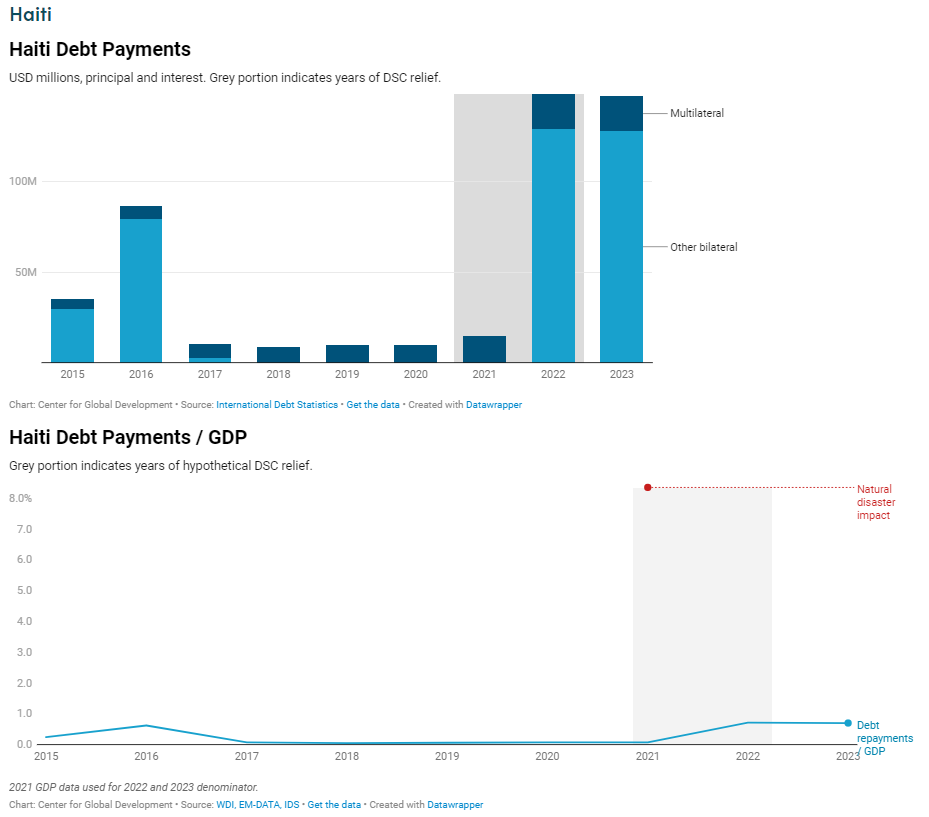

Haiti’s earthquake in 2021 inflicted 8.35 percent of GDP in economic damage. Haiti’s debt repayments are small owing to its small economy, lack of market access, and the fact that most assistance is in the form of grants. Its debt payments to all its creditors, both multilateral and bilateral creditors, accounted for less than 1 percent of GDP in 2022.

Takeaways

- DSCs are only relevant to a subset of countries under certain circumstances. DSCs have the potential to offer powerful financial buffers for some countries in an emergency. But they are not uniformly relevant. Predictably, DSCs offer the most financial relief for natural disaster-prone countries with high debt service levels. For countries like Haiti that mainly receive concessional loans and grants, DSCs will provide some relief, but not of the same magnitude as for more indebted countries. In these cases, the country itself should weigh the benefits of pursuing DSCs against the costs.

- DSCs are only useful if they are incorporated uniformly across all external creditors. If DSCs are to be a part of the LIC/LMIC toolkit, they will need to be included in MDB and bilateral loans, alongside commercial debt. For example, if they only had DSCs in MDB debt, relief would have been 1.4 percent of GDP for Mozambique and 1.5 percent for Pakistan. If DSCs were only in bonds, relief would have been 0.6 percent for Mozambique and 0.3 percent for Pakistan

- DSCs are not going to be useful for bonds with bullet repayments which is often the structure of choice for low-income countries and intermittent market issuers. In bullet repayments the entire principal comes due at the end of the life of the loan, making it ineligible for deferral. An amortizing structure, which is a feature of both Barbados and Grenada’s bonds, is much more relevant for DSCs, and allow for the postponement of principal repayment.

DSCs are not a comprehensive solution to the debt crisis, but they could have a significant impact in some countries. The challenge is to get major creditors to agree to a common set of standards and terms around DSCs—a tall order in an era where international cooperation is at a low point. MDBs are the largest creditors to much of the developing world so any effort to expand their use will likely require MDBs to adopt and champion them. But to be effective MDBs will need to make the inclusion of DSCs in their loans part of a broader effort to mainstream them across commercial and bilateral debt.

__________

[i] We excluded costlier disasters in China, India, and Brazil, given (a) these countries’ debt stocks are so large that comprehensively including DSCs across them would be impracticable, and (b) in the event of a large-scale natural disaster-related fiscal shock, these countries would likely issue additional debt or tap into other available sources of liquidity.

[ii] If the bonds of our sample countries had amortizing structures, we would have included principal repayments in the deferred amount, but this is not the case. Pakistan and Mozambique have bullet structured Eurobonds, and Haiti has no Eurobonds at all.

[iii] This figure is obtained by adding the fiscal space as a percentage of GDP in both years – 4.65% + 6.79% = 11.44%. The same is true of other fiscal relief estimates. We do this because we assume that debt relief would be front-loaded immediately following the crisis.

[iv] IDS data for Mozambique is dated and does not reflect the current payment schedule following the country’s 2019 restructuring. As a result, figures for Mozambique’s projected bond interest and principal payments were based on high level information published on Reuters following the restructuring deal – a $900 million dollar bond maturing in September 2031, with a 5 percent coupon until 2023, after which point the coupon would step up to 9%. A bullet payment structure is assumed, as that was the structure of its previous bond, and an amortizing structure was not otherwise noted. As a result, only interest payments feature in the debt service payment chart – $900 million at 5 percent, or $45 million a year. IDS data on other creditor types’ repayment schedules may also be out of date, but for consistency with other countries in the sample, we preserved IDS data.

Learn more