How We Can Put SDRs to Work in the Fight Against Climate Change—The Multilateral Development Bank Option

April 25, 2022

The world is in economic crisis and climate change is threatening our very existence. Many countries are in desperate need of financing to confront acute needs for energy and food, while at the same time facing huge investment costs to adapt to climate change and retool economies to low-carbon production.

In such times it should be unthinkable to leave any assets unused. But that is just what is happening now: Special Drawing Rights (SDRs) are sitting idle in many countries’ central banks. With a political push and some technical innovation, they can be put to good use at the multilateral development banks (MDBs) to accelerate the fight against climate change.

In a new, 90-second video we lay out how this could work:

Here’s the slightly, longer, more in-depth story:

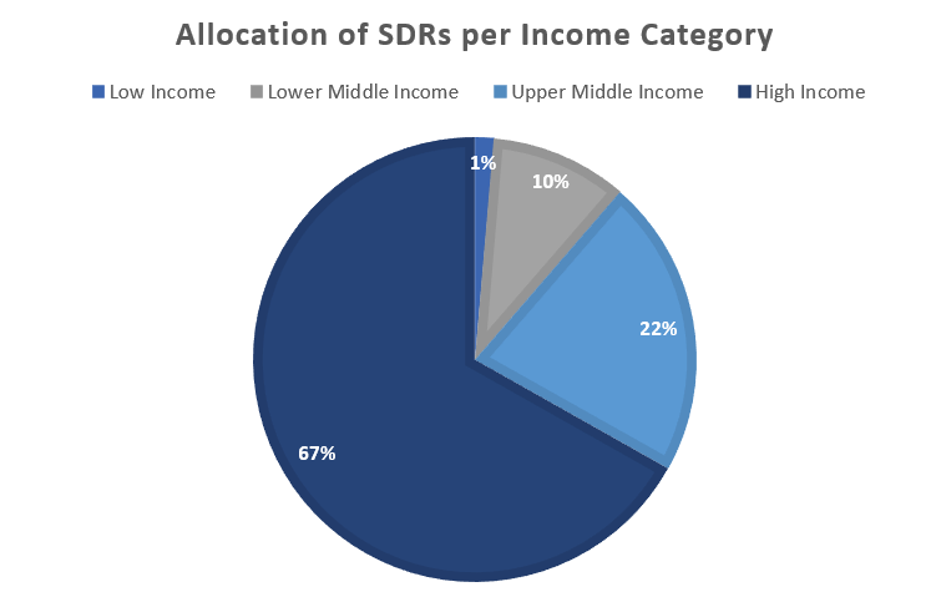

In August 2021, the International Monetary Fund issued $650 billion of Special Drawing Rights (SDRs) to the countries of the world. SDRs are not a currency, but they can be used to bolster countries foreign exchange reserves and provide a needed cushion against international economic shocks. Every country got a slice of the SDR pie, in proportion to their shareholding in the IMF.

While these emergency funds have proved very useful to low- and middle-income countries (LMICs) in confronting the economic aftermath of the COVID-19 pandemic, wealthier countries really didn’t need their SDRs. And most of the SDRs went to the wealthier countries and these funds are stuck in their central bank—providing extra cushioning where none is needed.

The international finance community has been looking for ways to use the SDRs of the wealthier countries to help LMICs in need of international reserves—a process called recycling. In late 2021, the G20 countries committed to recycling $100 billion of their SDRS. Much of this will be done by loaning SDRs back to the IMF, which will in turn lend them to LMICs through their Poverty Reduction and Growth Trust (PRGT) and the recently established Resilience and Sustainability Trust (RST). But the PRGT and RST cannot absorb $100 billion worth of SDRs. So wealthier countries are looking for other ways that SDRs can be used.

One promising avenue would be to recycle SDRs to the Multilateral Development Banks (MDBs)—institutions like the World Bank, the African Development Bank, the Asian Development Bank, the International Fund for Agricultural Development (IFAD), and others. There are several technical advantages to MDB recycling:

- The MDBs are highly rated financial institutions with a track record of helping LMICs mobilize financial resources.

- Most MDBs are so-called prescribed holders of SDRs, which means they can use them as a financial asset on their balance sheet and as a means of exchange with other international financial institutions and with countries.

- If the SDRs can be counted as capital, the MDBs can leverage the SDRs to mobilize additional funds for the private sector, thus multiplying the firepower of SDRs by as much as five times.

- Or the MDBs can just on-lend SDRs for specific purposes or in specific regions.

In the coming years, LMICs will have to adapt to the effects of climate change that we are already seeing by building new infrastructure, preparing for more frequent and severe climate events (hurricanes, floods, tsunamis). And like all the countries of the work LMICs will need to restructure their economies to be carbon neutral, which will involve huge changes in energy, agriculture, transportation, and many other sectors, all while continuing to invest in education, health, and social services.

And the MDBs can be the leaders in helping LMICs make these changes. Already the MDBs mobilized over $66 billion in 2020 alone and they must commit to doing more. SDRs can provide some of the capital needed to ramp up MDB lending to LMICS for climate change and other critical development tasks.

There are some obstacles to getting SDRs to the MDBs. Most SDRs are owned by central banks and provide a reserve cushion and central bankers want to be able to access that cushion if it is needed. The SDRs lodged at the MDBs will have to be structured in such a way that they could be accessed in an emergency. The IMF has structured the PRGT and RST so this is possible. Something similar can be done at MDBs—with a little technical innovation and flexibility.

But what is needed most right now is a political push to use SDRs at MDBs. Investing SDRs in MDBs is like using the money that you’ve saved for a rainy day to invest in a house. The house will give you protection for years to come, but if another disaster occurs you won’t have your rainy-day savings pot to help you out. In the international arena, it is a political decision how to use SDRs—as rainy-day funds (will worse days come?) or to build a sustainable future (if we don’t there will be no future?). Politicians can make this choice and it seems that investing in MDBs is like building a sturdy house to protect us from impending climate disaster.

Learn more