Maximising the developmental value of MDB callable capital: a new research agenda

June 6, 2023

How much can multilateral development banks (MDBs) lend?

This question is critical due to the central and systemic role of MDBs in tackling the many and multiplying global development challenges we face.

But the answer is far from simple, as the report of the G20’s Independent Review of Multilateral Development Bank Capital Adequacy Frameworks (2022) and ensuing discussions illustrate.

To help address this uncertainty, ODI with the support of the MDB Challenge Fund has launched a new research project to evaluate how MDBs can best make use of callable capital to underpin greater development lending.

While MDBs follow many of the basic lending principles common to for-profit commercial banks, they are also different in many important ways. As a result, standard capital adequacy guidelines for banks, like the Basel III framework, are not directly applicable. The risks faced by MDBs and the tools they have to deal with crises are fundamentally different.

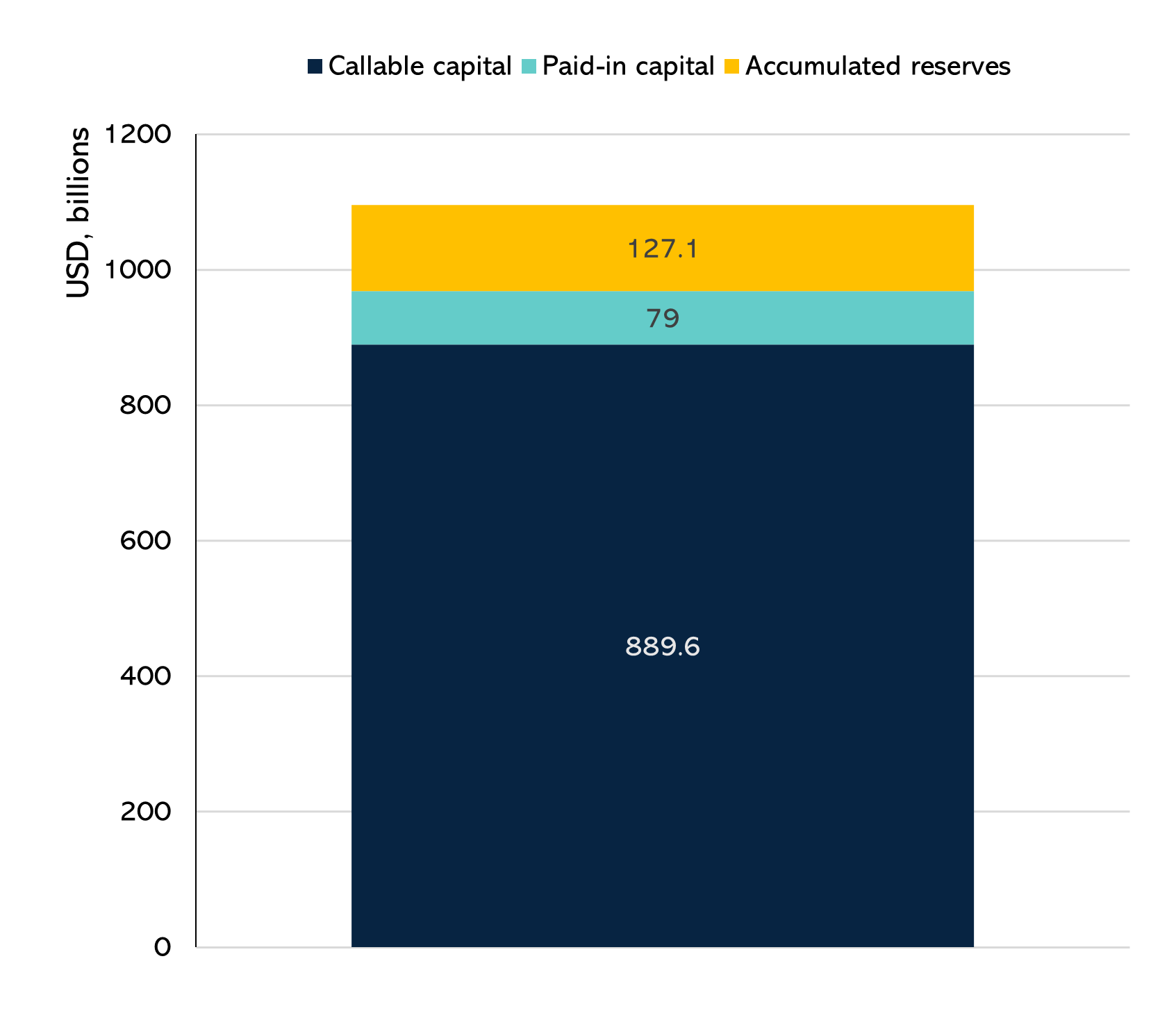

One key difference is their capital structure. Similar to commercial banks, MDB capital includes the cash capital paid in by member governments, plus accumulated retained earnings.

However, most MDBs also have very large amounts of callable capital. Callable capital is a special type of guarantee committed by government shareholders as a last resort for repaying debt obligations to bond holders in the event of an extreme shock to MDB finances. At the end of 2021, shareholders had subscribed $890 billion of callable capital in the seven MDBs considered in this study, over 10 times their $79 billion in regular paid-in capital.

Figure 1: Capital structure, selected MDBs

Source: 2021 financial statements of the African Development Bank, the Asian Development Bank, the Asian Infrastructure Investment Bank, the Development Bank of Latin America, the European Bank for Reconstruction and Development, the International Bank for Reconstruction and Development, and the Inter-American Development Bank.

Callable capital was created at Bretton Woods in 1944 as a tangible representation of the commitment of member governments to support the World Bank and thereby help build trust in the Bank’s creditworthiness among bond market actors. Callable capital was later replicated at other MDBs.

But what exactly is callable capital, and what is it worth? The uncomfortable truth is that no one is entirely sure. Despite the eye-popping nominal amounts, callable capital has never been called at any MDB, and the procedures for doing so are vague at best. It is also not obvious that all member governments could or would be willing to meet a call, for fiscal and political reasons, despite the fact that it is an international treaty commitment.

MDBs themselves – partly encouraged by the largest shareholders, who would be on the hook if a capital call occurred – have long managed their finances without reference to callable capital. As such, it is generally not included as an additional element of financial strength in internal MDB models of capital adequacy.

Credit rating agencies, by contrast, do give uplift for callable capital in their methodologies to rate MDB bonds. According to Standard & Poor’s, most of the large MDBs could lend substantially more and still be rated AAA, due to callable capital (see a 2020 report from ODI estimating headroom under S&P’s methodology). Moody’s and Fitch are less transparent, but also give considerable benefit for callable capital. The way the three agencies incorporate callable capital in their methodologies diverges widely, reflecting the ambiguities and uncertainties around this unusual instrument.

In an age of tremendous development finance needs, this confusion over a foundational pillar of the most important set of international development institutions is unacceptable. Callable capital may be worth less than the $890 billion nominal value, but it is certainly worth more than the zero value assigned to it by MDB capital adequacy models.

Callable capital is at its core a specialised type of instrument to absorb financial losses an MDB might face as a result of sudden, large-scale problems with loan repayment from borrowers, the likes of which have never yet affected any of the major MDBs. In fact, as an analysis for the G20 Independent Review demonstrates, MDBs have a superlative loan repayment record, far superior to commercial banks. Recognising callable capital’s financial benefits does not increase the risk profiles of MDB portfolios.

Despite this track record, it is important for MDBs, shareholders and rating agencies to understand what loss-absorbing instruments MDBs have to face a potential financial shock, just as with any lending institution. For callable capital to serve this purpose and be adequately valued by relevant stakeholders, key questions about its nature must be answered. These include how callable capital relates to other loss-absorbing instruments, the circumstances that can lead to a capital call, the process of a call, the ability of shareholders to meet a call and the purposes for which the resources can be used.

A better understanding of callable capital’s value could result in a substantial increase in available lending headroom, within an overall framework of long-term financial sustainability and a AAA bond rating. This is an essential step in modernising the MDB financial model to face the challenges of the coming decades.

This ODI research project directly addresses these issues. It was among the first recipients of funding announced by the MDB Challenge Fund at the 2023 Spring Meetings of the World Bank and International Monetary Fund. Preliminary research findings are expected by October 2023, and the final results by end-April 2024. For more details on the project team and research components, see the Annex below.

Learn more